http://www.dailyfx.com/forex/fundamental/article/what_fed_watches/2011/01/07/Dollar_Rally_May_be_Short-Lived_without_Risk_Trends_to_Back_It.html

Be sure to join DailyFX Analysts in discussing their outlook for the Fed and its impact on the dollar in the DailyFX Forex Forum

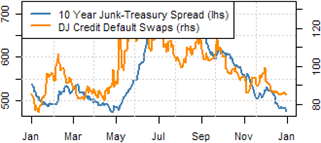

| Credit Market | Previous | Current | Change | % Change | Outlook * |

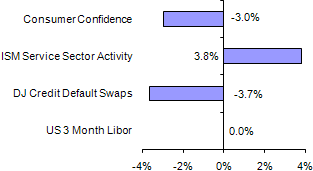

| DJ Credit Default Swaps | 85.350 | 82.230 | -3.120 | -3.66% | Improving |

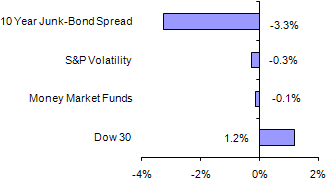

| 10 Year Junk-Bond Spread | 482.71 | 466.90 | -15.81 | -3.28% | Improving |

| Credit Card Delinquencies | 4.28 | 4.15 | -0.13 | -0.13% | Improving |

| Mortgage Delinquencies | 9.85 | 9.13 | -0.72 | -0.72% | Improving |

| US 3 Month Libor Rate | 0.303 | 0.303 | 0 | 0.00% | Deteriorating |

| Total Money Market Funds | 2813.61 | 2810.23 | -3.38 | -0.12% | Improving |

| Stock Market | Last Week | Current | Change | % Change | Outlook |

| Dow Jones Industrial Average | 11585.38 | 11722.89 | 137.51 | 1.19% | Improving |

| Dow Jones Real Estate Index | 217.44 | 217.91 | 0.47 | 0.22% | Improving |

| Dow Jones Financial Index | 371.19 | 380.8 | 9.61 | 2.59% | Improving |

| Dow Jones Retail Index | 89.58 | 89.77 | 0.19 | 0.21% | Improving |

| S&P Volatility | 17.28 | 17 | -0.28 | -0.28% | Improving |

| Put-Call Ratio | 1.45 | 1.5 | 0.05 | 0.05% | Deteriorating |

| Market Breadth (Adv - Dec) | 0.5377 | 0.5641 | 0.0264 | 2.64% | Improving |

| Economic Indicators | Previous | Current | Change | % Change | Outlook |

| GDP (Annualized) | 2.8 | 2.6 | 2.6 | 2.60% | Improving |

| Mortgage Applications | -3.9 | 2.3 | 2.3 | 2.30% | Improving |

| Initial Jobless Claims | 410 | 388 | -22 | -5.37% | Improving |

| Consumer Confidence (CB) | 54.1 | 52.5 | -1.6 | -2.96% | Deteriorating |

| ISM Manufacturing | 56.6 | 57 | 0.4 | 0.71% | Deteriorating |

| ISM Services | 55 | 57.1 | 2.1 | 3.82% | Deteriorating |

| ISM Services - Employment | 52.7 | 50.5 | -2.2 | -4.17% | Deteriorating |

An Improving outlook means the Federal Reserve coulduse thisindicator

to support a rate hike. The opposite stands for a deteriorating outlook.

The Economy and the Dollar

Abnormal market conditions through the turn of the year have certainly had a warping effect on the US dollar. Through the final days of trading through 2010, a tumble from the greenback that was independent of other speculatively-guided asset classes pushed the currency on its worst run in a month. And, naturally, the opening days of 2011 would see the biggest rally in a month. It is difficult to attribute how much of this volatility can be attributed to the withdrawal and subsequent infusion of capital into the capital markets; but it is worth comparing this currency’s performance to counterparts within the FX market and outside of it. First of all, it should be noted that despite the greenback’s remarkable performance, the Japanese yen and Swiss franc have both plunged. At the same time, the S&P 500 (our normal benchmark for risk appetite) has maintained its steady but tempered climb while the Australian dollar (a favored high-yield currency) has stumbled right alongside the yen. It could be that the dollar itself is simply very strong in the face of underlying trends. However, these marked drop in anticipated correlations likely points to ongoing distortions. All things considered, liquidity issues won’t take very long to clear up. Alternatively, the warping of risk appetite through unnatural stimulus flows in the US, Europe and Asia could keep speculation artificially inflated indefinitely. That said, there are natural limits to how much money can be forced into the system before economic and financial markets start to breakdown. This is perhaps why we have seen a slow shift towards austerity recently. When the government withdrawal really picks up momentum, we will see just how confident investors really are in the future.

A Closer Look at Financial and Consumer Conditions

It is hard to assess risk when market conditions are distorted by liquidity. Yet, there are signals from around the market that should make any trader leery of what the future holds. The first concern is speculative activity itself. If the S&P 500 is a benchmark for risk appetite, then many believe it is a promising sign that the index is carving a remarkably restrained and consistent advance. However, a normally functioning market should reflect the shifting tides of confidence that are normal to a crowd. What makes it even more irregular are the fundamental developments over the past weeks. While data hasn’t shown any extraordinary fluctuations; financial concerns in US housing, Chinese inflation and European sovereign funding are critical concerns. |  The US economy is improving. While many unemployed Americans may refute this claim, the Federal Open Market Committee’s (FOMC) minutes from its last policy meeting noted the majority of the nation’s districts were reporting some level of improvement. Though, it is worth stating that this growth was not substantial enough to alter their plans for executing the full $600 billion stimulus program announced back in November. Looking at the economic data for a more objective assessment, there are signs that mark the path to recovery. Most recent was the seven month high in the ISM manufacturing report and four-and-a-half year high for its service sector survey. However, a true recovery (for the US and perhaps the globe) depends on the US consumer. Employment and spending are still notable absent ingredients. |

The Financial and Capital Markets

Risk appetite trends are difficult to get a bead on. With the typical correlations between the various speculative asset classes breaking down, it is fair to suggest that investor confidence is not a primary catalyst – or at least that there is not enough consistency in opinion to unify the markets. Does this mean that a new regime is upon us? Perhaps pricing has finally evolved into the efficient market that academics have long been waiting for? Unlikely. Speculators are still a driving force and they are as prone to greed and panic as they were six months ago, a year ago or 10 years ago. What is needed is an event to spark speculative interests and encourage the wholesale transfer of capital from one corner of the market to another. Friday’s NFPs can prove to be just such a catalyst. Already a well-known and closely watched report, this indicator has been made all the more remarkable because of a proprietary ADP payroll report encouraging expectations a government reading that could climb as high as half a million jobs. This could be the source of a deeper sense of optimism; but it also makes it far easier to disappoint. If this particular indicator fails to do the job; it likely means that sentiment will have to be realigned via an exogenous and overpowering development. That being the case, it is becoming more and more difficult to encourage optimism when prices are already so rich.

A Closer Look at Market Conditions

Steady and blissfully ignorant. That is the best description for the capital market benchmarks. A bull trend is not something to be inherently suspicious of; but an advance that has barely corrected or even temporarily exhausted its climb is. Though it is intangible, there is always a level of fair value for each market and asset. That means to facilitate a steady climb, fair value must consistently be seen higher than the prevailing price. Yet, that is a difficult scenario to reconcile with the questionable fundamentals behind the US and global economic recoveries and the existence of so many potential financial disruptions. Reality will dawn, eventually. |  Risk seems to be the farthest thing from investors’ minds. The consistent advance of the S&P 500 seems to have lulled the cautious into passivity. Looking at the VIX for the benchmark stock index (a measure of insurance cost for adverse scenarios developing through the near future), we can see the favored measure for risk is skipping along its lowest levels since before the global financial crisis erupted. We certainly aren’t facing the same risks that we were back then (though we couldn’t tell that was the case back then either). Yet, given that the masses are keenly aware of the troubles developing with European financing, Chinese inflation and US housing; it is somewhat unnerving that they are not preparing for contingencies. |

Written by: John Kicklighter, Currency Strategist for DailyFX.com

To receive John’s reports via email or to submit Questions or Comments about an article; email jkicklighter@dailyfx.com

DailyFX provides forex news on the economic reports and political events that influence the currency market.

Learn currency trading with a free practice account and charts from FXCM.

Learn currency trading with a free practice account and charts from FXCM.

No comments:

Post a Comment