http://www.dailyfx.com/forex/fundamental/daily_briefing/session_briefing/us_open/2011/01/07/Euro_Weakness_Persists_U.S._Dollar_to_Face_Increased_Volatility.html

Talking Points

- British Pound: Maintains Downward Trend

- Euro: 3Q GDP Expands Less-Than-Expected

- Canadian Dollar: Employment Expands For Third Month

- U.S. Dollar: Non-Farm Payrolls, Consumer Credit on Tap

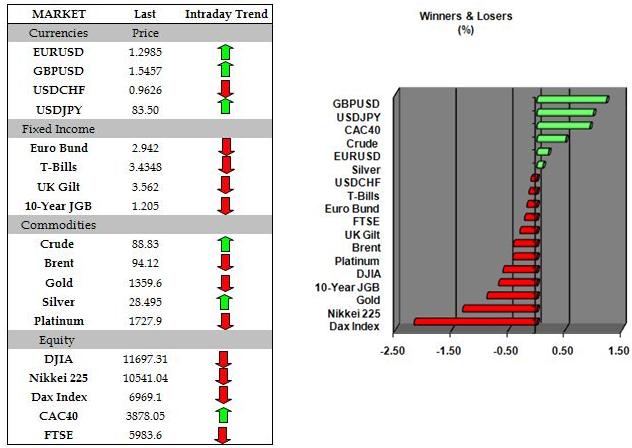

The EUR/USD slipped to a fresh monthly low of 1.2960 during the overnight trade, and the exchange rate may continue to retrace the advance from back in September as fears surrounding the European debt crisis intensify. European Central Bank President Jean-Claude Trichet said the governments operating under the fixed-exchange rate system must be “more ambitious” in managing their public finances, and went onto say that “monetary policy responsibility cannot substitute for government irresponsibility” while speaking in front of German policy makers.

As the ECB struggles to restore investor confidence, the central bank could be forced to delay its exit strategy further, and the Governing Council may look to support the real economy throughout the first-half of 2011 as policy makers expect to see an uneven recovery going forward. Nevertheless, the final GDP reading for the Euro-Zone showed the growth rate expanded 0.3% in the third quarter amid an initial forecast for a 0.4% expansion, while a separate report showed unemployment held at the record-high of 10.1% for the second consecutive month in November. As the tough austerity measures bear down on the recovery, the ECB is likely to retain a dovish tone for future policy, and the central bank may push its primary mandate to ensure price stability to the backburner as the ongoing slack within the real economy dampens the outlook for inflation.

The British Pound bounced back from a low of 1.5405 during the European trade, but the small correction in the exchange rate is likely to be short-lived as the GBP/USD maintains the downward trend carried over from the previous year. Meanwhile, former Bank of England board member David Blanchflower talked down speculation for a rate hike this year and said higher borrowing costs would be the “worst nightmare” forChancellor of the Exchequer George Osborn as the private sector remains weak, and went onto say that the MPC should maintain its wait-and-see approach “for a while” during an interview with Bloomberg Television. However, as the BoE forecasts inflation to hold above the 2% target this year, there is likely to be a growing split within the MPC, and members of the committee may struggle to meet on common ground as the economic outlook remains clouded with uncertainties.

U.S. dollar price action was mixed for the second day, with the USD/JPY advancing to a high of 83.58, and the greenback is expected to face increased volatility going into the North American trade as the economic docket is expected to reinforce an improved outlook for future growth. U.S. non-farm payrolls are forecasted to increase another 150K in December following the 39K rise in the previous month, while the annual rate on unemployment is expected to fall back to 9.7% from 9.8% as labor conditions improve. However, there could be a mixed reaction to the data as the holiday season typically boosts demands for temporary workers, and the underlying weakness in the labor market may continue to dampen the prospects for a sustainable recovery as private sector consumption remains one of the leading drivers of growth. Moreover, consumer credit in the world’s largest economy is expected to expand another $0.5B in November after expanding $3.4B in the month prior, while Fed Chairman Ben Bernanke is scheduled to testify in front of the Senate Budget Committee at 14:30 GMT on monetary and fiscal policy. In turn, comments from the central bank head could spark whipsaw price action in the currency market, and Mr. Bernanke is likely to maintain a cautious tone for the economy as the fundamental outlook remains clouded with high uncertainty.

Related Articles: Forex Weekly Trading Forecast - 01.03.11

FX Upcoming

| Currency | GMT | EST | Release | Expected | Prior | ||

| USD | 13:30 | 08:30 | Change in Non-farm Payrolls (DEC) | 150K | 39K | ||

| USD | 13:30 | 08:30 | Change in Manufacturing Payrolls (DEC) | 5K | -13K | ||

| USD | 13:30 | 08:30 | Unemployment Rate (DEC) | 9.7% | 9.8% | ||

| CAD | 13:30 | 08:30 | Average Hourly Earnings (MoM) (DEC) | 0.2% | 0.0% | ||

| CAD | 13:30 | 08:30 | Average Hourly Earnings (YoY) (DEC) | 1.8% | 1.6% | ||

| CAD | 13:30 | 08:30 | Average Weekly Hours (DEC) | 34.3 | 34.3 | ||

| CAD | 13:30 | 08:30 | Change in Private Payrolls (DEC) | 175K | 50K | ||

| Currency | GMT | Release | Expected | Actual | Comments |

| CHF | 06:45 | Unemployment Rate (DEC) | 3.7% | 3.8% | Highest since May. |

| CHF | 06:45 | Unemployment Rate s.a. (DEC) | 3.5% | 3.6% | Holds steady for third month. |

| EUR | 07:00 | German Retail Sales (MoM) (NOV) | 1.0% | -2.4% | Biggest decline since March 2008. |

| EUR | 07:00 | German Retail Sales (YoY) (NOV) | 3.0% | 2.0% | |

| EUR | 07:00 | German Trade Balance (euros) (NOV) | 15.0B | 12.9B | Trade surplus slips to a three-month low, led by fading demands for exports. |

| EUR | 07:00 | German Current Account (euros) (NOV) | 15.5B | 12.0B | |

| EUR | 07:00 | German Exports (MoM) (NOV) | 1.0% | 0.5% | |

| EUR | 07:00 | German Imports (MoM) (NOV) | 1.6% | 4.1% | |

| EUR | 07:45 | French Trade Balance (euros) (NOV) | -- | -3.9B | Deficit widens on higher imports. |

| GBP | 08:58 | New Car Registrations (YoY) (DEC) | -- | -18.0% | Weakens for the sixth month. |

| EUR | 09:00 | Italian Unemployment Rate s.a. (NOV) | 8.6% | 8.7% | Holds steady for second month. |

| EUR | 10:00 | Euro-zone GDP (QoQ) (3Q) | 0.4% | 0.3% | The downward revision comes as the government withdraws fiscal support. Business spending contracts for second time in 2010. |

| EUR | 10:00 | Euro-zone GDP (YoY) (3Q) | 1.9% | 1.9% | |

| EUR | 10:00 | Euro-zone Gross Fixed Capital (QoQ) (3Q) | 0.0% | -0.3% | |

| EUR | 10:00 | Euro-zone Household Consumption (QoQ) (3Q) | 0.3% | 0.1% | |

| EUR | 10:00 | Euro-zone Unemployment Rate (NOV) | 10.1% | 10.1% | |

| EUR | 10:00 | Euro-zone Govt Expenditure (QoQ) (3Q) | 0.4% | 0.4% | |

| EUR | 11:00 | German Industrial Production n.s.a w.d.a (YoY) (NOV) | 10.9% | 11.1% | Contracts for the fourth time in 2010. |

| EUR | 11:00 | German Industrial Production (MoM) (NOV) | -0.1% | -0.7% | |

| CAD | 12:00 | Net Change in Employment (DEC) | 20.0K | 22.0K | Largest advance since August, unemployment holds steady as discouraged workers leave the labor force. |

| CAD | 12:00 | Part Time Employment Change (DEC) | -- | -16.1K | |

| CAD | 12:00 | Full Time Employment Change (DEC) | -- | 38.0K | |

| CAD | 12:00 | Participation Rate (DEC) | 67.0 | 66.9 | |

| CAD | 12:00 | Unemployment Rate (DEC) | 7.7% | 7.6% |

DailyFX provides forex news on the economic reports and political events that influence the currency market.

Learn currency trading with a free practice account and charts from FXCM.

Learn currency trading with a free practice account and charts from FXCM.