http://www.dailyfx.com/forex/fundamental/article/special_report/2011/01/21/China_Begins_to_Sacrifice_Trade_Surplus_to_Stem_Inflation.html

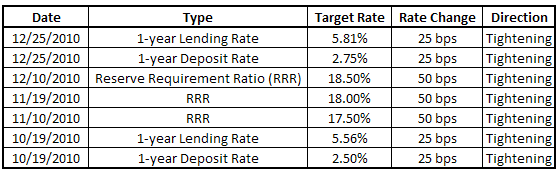

While one Asian titan has faced severe deflationary pressures for the better part of the past decade, implications for Japan’s neighbor to the west, China, are diametrically opposite. In fact, inflation has become such a concern for the emerging economy that the People’s Bank of China has had to raise rates across various mediums – not just the main reserve requirement ratio, but also on specific 1-year lending and deposit rates for certain sized banks – a few times during the course of 2010 in order to stem inflationary fears, which would cause an appreciation for the Yuan as interest rates rise.

While the People’s Bank of China does not release information on monetary policy, market sentiment indicates that two or three more rate hikes could be expected, and when they do, the Dollar will suffer mightily. However, any Yuan strength will come to fruition slowly, as currently, the People’s Bank of China only allows the Yuan to fluctuate by up to 0.5 percent on either side of the central parity rate, now at 6.5883. While trading the Yuan is limited to institutional investors, retail traders can still expose themselves to Yuan strength through other outlets. Given the trade relationships that China has with Australia and New Zealand, interest rate hikes by the People’s Bank of China have translated into declines by the Aussie and the Kiwi versus the Dollar. Accordingly, going forward, shorting the Aussie or Kiwi, particularly against the U.S. Dollar, looks to be profitable when China raises its interest rates.

Early reports indicate that the People’s Bank of China is willing to let the Yuan appreciate as much as 5 percent against the U.S. Dollar in 2011; the Yuan appreciated by approximately 4.2 percent against the Greenback in 2010. Recent commentary by the People’s Bank of China – that the inflation situation remains “not optimistic” – indicate that should an intervention arrive in 2011, it will arrive in early 2011.

The People’s Bank of China’s concurring decisions to raise rates have been predicated on the necessity to contain food and housing prices. China’s Consumer Price Index has been positive since November 2009, and according to the most recent CPI release on January 20, 2011, inflation grew at a 4.6 percent clip after beating expectations in December, which showed inflation grew at a 5.1 percent pace; the People’s Bank of China aims to maintain an inflation rate of 3 percent. The People’s Bank of China effort is a clear confirmation that inflation is a real concern, and thus rate hikes will be necessary to keep economic growth on a stable trajectory; China will intervene on some indirect level.

Unlike Japan, China’s economy has not suffered from the effects of the global pullback: third quarter GDP was 9.6 percent on a year-over-year basis, and fourth quarter GDP was 9.8 percent. Similarly, exports outpaced Imports in November, 34.9 percent to 25.3 percent, respectively. As such, China has the ability to let its trade surplus suffer slightly at the expense of cooling inflation. An appreciation of the Yuan would make imports cheaper, reducing the impact of rising commodity and food prices. The recent rate hikes may have already had this affect: exports expanded by 17.9 percent in December, while Imports grew at 25.6 percent: the trade balance surplus narrowed to $13.1 billion from $22.89 billion in November.

Written by Christopher Vecchio, DailyFX Research

To contact the author, please send inquiries to: cvecchio@fxcm.com

DailyFX provides forex news on the economic reports and political events that influence the currency market.

Learn currency trading with a free practice account and charts from FXCM.

Learn currency trading with a free practice account and charts from FXCM.

No comments:

Post a Comment