http://www.dailyfx.com/forex/fundamental/article/what_fed_watches/2011/01/21/Dollar_Slowly_Weighed_by_Risk_Stimulus_Euro.html

Be sure to join DailyFX Analysts in discussing their outlook for the Fed and its impact on the dollar in the DailyFX Forex Forum

| Credit Market | Previous | Current | Change | % Change | Outlook * |

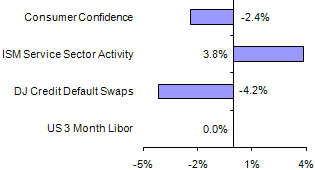

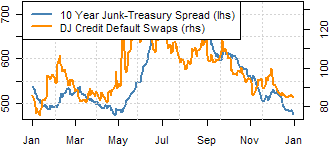

| DJ Credit Default Swaps | 86.003 | 82.429 | -3.574 | -4.16% | Improving |

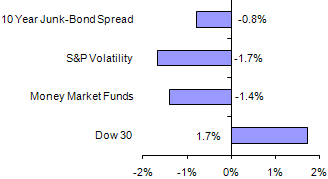

| 10 Year Junk-Bond Spread | 459.35 | 455.75 | -3.6 | -0.78% | Improving |

| Credit Card Delinquencies | 4.15 | 3.91 | -0.24 | -0.24% | Improving |

| Mortgage Delinquencies | 9.85 | 9.13 | -0.72 | -0.72% | Improving |

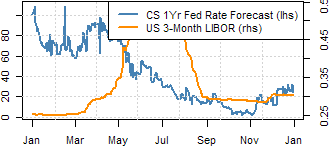

| US 3 Month Libor Rate | 0.303 | 0.303 | 0 | 0.00% | Deteriorating |

| Total Money Market Funds | 2835.77 | 2796.47 | -39.3 | -1.39% | Improving |

| Stock Market | Last Week | Current | Change | % Change | Outlook |

| Dow Jones Industrial Average | 11637.45 | 11837.93 | 200.48 | 1.72% | Improving |

| Dow Jones Real Estate Index | 216.17 | 220.99 | 4.82 | 2.23% | Improving |

| Dow Jones Financial Index | 377.48 | 389.82 | 12.34 | 3.27% | Improving |

| Dow Jones Retail Index | 88.98 | 90.79 | 1.81 | 2.03% | Improving |

| S&P Volatility | 17.54 | 15.87 | -1.67 | -1.67% | Improving |

| Put-Call Ratio | 1.59 | 1.48 | -0.11 | -0.11% | Improving |

| Market Breadth (Adv - Dec) | 0.4346 | 0.6249 | 0.1903 | 19.03% | Improving |

| Economic Indicators | Previous | Current | Change | % Change | Outlook |

| GDP (Annualized) | 2.8 | 2.6 | 2.6 | 2.60% | Improving |

| Mortgage Applications | 2.3 | 2.2 | 2.2 | 2.20% | Improving |

| Initial Jobless Claims | 423 | 445 | 22 | 5.20% | Deteriorating |

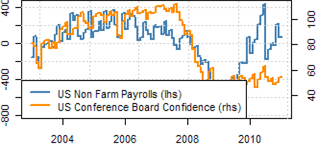

| Consumer Confidence (CB) | 74.5 | 72.7 | -1.8 | -2.42% | Deteriorating |

| ISM Manufacturing | 56.6 | 57 | 0.4 | 0.71% | Deteriorating |

| ISM Services | 55 | 57.1 | 2.1 | 3.82% | Deteriorating |

| ISM Services - Employment | 52.7 | 50.5 | -2.2 | -4.17% | Deteriorating |

An Improving outlook means the Federal Reserve coulduse thisindicator

to support a rate hike. The opposite stands for a deteriorating outlook.

The Economy and the Dollar

There are times when a currency is the master of its own destiny; but more often than not, larger fundamental themes overshadow those innate developments that lull many into expecting a straightforward path. This is the condition that the dollar now finds itself in. While, it could be said that the greenback has leveraged its strength and weakness primarily through its role as a liquid safe haven, we can see these drivers have started to firm up substantially this past week. Acting as a constant pressure, risk appetite has extended the S&P 500’s consistent advance to scale heights not seen in over two years. And yet, consistent as the climb may be; the conviction in this bearing is noticeably flimsy. This leaves the responsibility of substantial dollar selling to fall to another major function of the benchmark currency: acting as the primary counterpart to the euro. Just as surely as this role helped the dollar gain ground when the Ireland bailout accelerated a deterioration of market conditions; the subsequent suite of proposals aimed at stabilizing the Euro-area’s finances have leveraged a euro (and therefore dollar) correction. Looking forward, the euro’s indirect influence will remain a dominant force behind the dollar’s performance. Yet, we should also consider the impact that native event risk could have on the currency as well. The FOMC rate decision can tap into speculation surrounding the warping stimulus efforts; while the advanced reading of 4Q GDP can revive an interest in comparative growth (or perhaps leverage risk appetite).

A Closer Look at Financial and Consumer Conditions

Financial market conditions seem to have improved substantially over the past few weeks. Aside from the taste of risk appetite seen in many of the capital market benchmarks; we have seen a couple of the global market’s biggest threats temper. At the top of list for concern, European Union officials have made open-ended promises for boosting support of their financial system. And, while the likelihood of the most critical proposals finding a popular vote is low; the crowd’s bloodlust has been satisfied for now. From China, the strong 4Q GDP numbers have temporarily offset concerns that the additional measures will likely be taken to cool inflation. And, in the US, a relatively strong 4Q earnings season so far has pushed back the threat of remuneration for stimulus for the time being. |  US economic data crossing the wires over the past week has produced a modest impact on the dollar itself. However, the influence on the appetite for risk has once again proven itself to be meaningful. Among the highlights were a drop in the trade deficit, the sixth consecutive monthly rise in retail sales, a strong industrial production figure and a surge in existing home sales. And, while the University of Michigan consumer sentiment survey would slip somewhat from the previous reading, it was still well into positive territory. The net effect: we are seeing the evidence of a slow but true recovery. That said, the cumulative influence of all the data from this past week will not measure up to the single report of the advanced 4Q GDP reading. Growth is essential for return; but it is also the a prerequisite for withdrawing stimulus. |

The Financial and Capital Markets

The markets have driven the proliferation of risk appetite even further this past week. However, deviation in a few key places draws concern that fundamental conviction may be less durable than the S&P 500’s climb would suggest. If we were to look solely at the benchmark US indexes; we would be left with the impression that there is little question about conviction. However, it is important to maintain a global macro perspective when there are distorting factors like stimulus that need to be accounted for. It should strike any investor as concerning that the Chinese equity market is itself is at three-month lows; because this particular economy has stood as a benchmark for what optimal returns could be had given current global conditions. And, back in the US, we have seen earnings take center stage. And, once again, the results seem generally promising. For the most part, financial and general industry benchmarks seem to be booking meaningful profit despite a dependency of stimulus and unquestionable lack of domestic demand. A year ago, the numbers alone would be enough to drive risk-taking efforts. However, skepticism is starting to seep in. Creative accounting and reliance on temporary factors (government aid, a cheap currency as a subsidy, emerging market demand) will not be able to sustain the world’s largest economy through a true multi-year growth phase. Yet speculators will be happy to take advantage of cheap capital and stimulus-led returns as long as they can.

A Closer Look at Market Conditions

The general trend between physical and financial assets remained relatively tight through the past few weeks. This in itself is an oddity though considering commodity inflation necessarily degrades growth. This simply fundamental reality, however, must fight the forced interest in risk appetite that keeps capital seeking out the highest return. For the benchmark S&P 500, 28-month highs were tested intra-week and crude marked its own relative high. And, though a late week correction seems as if it may shake some long-term sense into market participants; the draw of high returns will likely keep the larger trends in place. |  Checking the standard measures of risk, we continue to see a market content on maintaining their yield-bearing positions with comparatively little regard for the risks it involves. From the S&P 500-based VIX, lows last seen in 2007 are just in sight while the currency equivalent slipped to four-month lulls of its own. In the meantime, even credit default swap spreads have shown marked improvement in Europe (which happens to be one of the most threatening areas for global finance). It should be remembered that the need for protection from risk exposure is at its highest when the markets are at their zenith. Yet, that is inevitably the time when trades try to squeeze as much leverage out as they can for greater returns. |

Written by: John Kicklighter, Currency Strategist for DailyFX.com

To receive John’s reports via email or to submit Questions or Comments about an article; email jkicklighter@dailyfx.com

DailyFX provides forex news on the economic reports and political events that influence the currency market.

Learn currency trading with a free practice account and charts from FXCM.

Learn currency trading with a free practice account and charts from FXCM.

Trade Stocks, Forex, And Bitcoin Anywhere In The World: Ic Markets Is The Leading Provider Of Software That Allows You To Trade On Your Own Terms. Whether You Are Operating In The Forex, Stock, Or Cryptocurrency Markets, Use Meta Fx Global's Software And Anonymous Digital Wallet To Connect With The Financial World.: Myfxglobal Is A Currency Trading Company That Allows You To Trade Stocks, Forex, And Cryptocurrency.

ReplyDelete