http://www.dailyfx.com/forex/fundamental/article/what_fed_watches/2010/12/30/Dollar_Traders_Looking_Ahead_to_True_Volatility_Trends_in_2011.html

Be sure to join DailyFX Analysts in discussing their outlook for the Fed and its impact on the dollar in the DailyFX Forex Forum

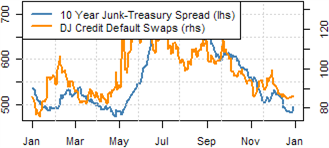

Credit Market | Previous | Current | Change | % Change | Outlook * |

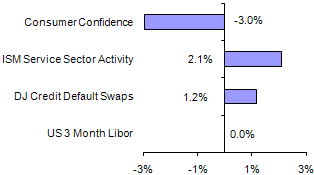

DJ Credit Default Swaps | 84.750 | 85.750 | 1.000 | 1.18% | Deteriorating |

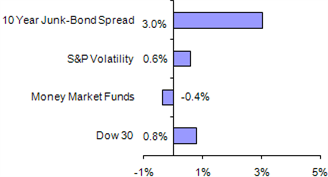

10 Year Junk-Bond Spread | 484.04 | 498.66 | 14.62 | 3.02% | Deteriorating |

Credit Card Delinquencies | 4.28 | 4.15 | -0.13 | -0.13% | Improving |

Mortgage Delinquencies | 9.85 | 9.13 | -0.72 | -0.72% | Improving |

US 3 Month Libor Rate | 0.303 | 0.303 | 0 | 0.00% | Deteriorating |

Total Money Market Funds | 2797.97 | 2787.9 | -10.07 | -0.36% | Improving |

Stock Market | Last Week | Current | Change | % Change | Outlook |

Dow Jones Industrial Average | 11533.16 | 11622.46 | 89.3 | 0.77% | Improving |

Dow Jones Real Estate Index | 213.96 | 217.09 | 3.13 | 1.46% | Improving |

Dow Jones Financial Index | 369.27 | 371.64 | 2.37 | 0.64% | Improving |

Dow Jones Retail Index | 88.08 | 89.45 | 1.37 | 1.56% | Improving |

S&P Volatility | 16.49 | 17.09 | 0.6 | 0.60% | Deteriorating |

Put-Call Ratio | 1.92 | 1.45 | -0.47 | -0.47% | Improving |

Market Breadth (Adv - Dec) | 0.5250 | 0.5698 | 0.0448 | 4.48% | Improving |

Economic Indicators | Previous | Current | Change | % Change | Outlook |

GDP (Annualized) | 2.8 | 2.6 | 2.6 | 2.60% | Improving |

Mortgage Applications | -2.3 | -18.6 | -18.6 | -18.60% | Deteriorating |

Initial Jobless Claims | 441 | 420 | -21 | -4.76% | Improving |

Consumer Confidence (CB) | 54.1 | 52.5 | -1.6 | -2.96% | Deteriorating |

ISM Manufacturing | 56.9 | 56.6 | -0.3 | -0.53% | Deteriorating |

ISM Services | 54.3 | 55 | 0.7 | 1.29% | Deteriorating |

ISM Services - Employment | 50.9 | 52.7 | 1.8 | 3.54% | Deteriorating |

An Improving outlook means the Federal Reserve could use this indicator

to support a rate hike. The opposite stands for a deteriorating outlook.

The Economy and the Dollar

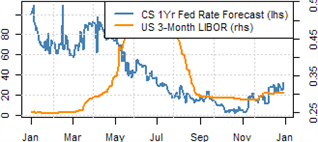

The effects of thinned speculative interest and year-end position squaring are having their influence on the benchmark dollar. Like most other asset classes, the sway of risk appetite trends and other fundamental drivers have been curbed by the shared belief amongst market participants that significant developments do not take place in the final weeks of the year. This is a state of reality that is only supported by popular opinion - which is ultimately the same definition of a market itself. Therefore, there is the potential of a significant trend taking root through the remainder of 2010; but that is a low probability scenario. More likely, the investing masses await the new year to decide what regions / markets have the best potential and thus where they should allocate their capital. By this time next week, we will be in the new trading year; but expecting an abrupt return to active market conditions is excessive. The return of liquidity will likely take some time; but the broader fundamental trends ahead for the dollar are laid out. Stimulus will be an ongoing source of pain for the value of the greenback. The Fed has laid out the $600 billion target for the second round of easing; and the policy authority has increased its balance sheet by $124.8 billion through last week. A lack of ambiguity means this effort is already fairly priced in; but speculation of ending the program early or carrying it further will slowly bleed in. The greater concern in the early weeks of January will be the underlying sense of risk appetite. The S&P 500 (a good benchmark for risk appetite) has consistently advanced since September; but without the benefit of solid fundamentals. This is a high risk trend - one where a correction would distinctly benefit the dollar.

A Closer Look at Financial and Consumer Conditions

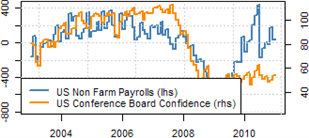

The financial markets may be quieter; butthey certainly aren’t any more stable. With speculators taking a rest, volatility will be constrained to smaller ranges and trends will be curbed. As for the true sentiment behind the markets, there has been a steady outflow of retail interest from the capital markets and there are distinct risks on the horizon. For the US, unemployment may be the top concern for those measuring the influence of stimulus; but the risk of a crisis is more distinct in the risk of a second housing collapse. Home values will continue to deteriorate as demand is depressed through wages and employment and supply is bolstered by foreclosures. Yet, it is important to recognize that the backlog of foreclosures and refinancing may pose a deeper threat. |  Should we follow what consumers say or do? This was the question posed after the Conference Board’s consumer confidence survey for December was released this past week. An unexpected drop in the headline figure contrasted the six-month high in the University of Michigan counterpart as well as the report that holiday spending this year was at its highest level in five years. Looking at the details of this useful report, we see a modest drop in plans to make major purchases; but the real impact was felt in employment statistics. Not surprising. The US economy is currently heavily supported by stimulus; and yet the payoff is still relatively small. Some economists are calling for a ‘muddle-through’ 2011; but such a scenario could prove extremely risky as another shock could leave policymakers short on options. |

The Financial and Capital Markets

We are in the pull of the year-end seasonal effect across the financial markets. Over the past few years, this hasn’t curbed the influences of volatility (but that was the exception given the aggressive rebound from the worst financial crisis in recent history and the unusual capital flows through the end of 2009). This time around, conditions are still somewhat unusual. Typically a time to offset positions and stick to the sidelines, we are actually seeing the benchmarks for speculative interest are maintaining a steady advance – albeit at a slower clip. Part of this performance can be associated to a natural market flow associated to traders cover their speculative shorts. The participation in the equity market’s rally particularly has seen relatively little participation from the retail investment community (instead finding fuel from redirected stimulus injections). On the other hand, we have seen a significant build up of speculative shorts through August that have been falling off ever since. With another push to unwind short positions this past week, we see that such bearish positions are at their lowest levels since the beginning of the year. And, a direct result of this effort to offset shorts happens to be a bid that would seem to match the slow pace of advance that the benchmark S&P 500 has maintained.

A Closer Look at Market Conditions

If we removed ourselves from any thought of fundamentals or financial valuation, it would seem that the capital markets are in their most robust period of performance in years. The Dow Jones Industrial Average and S&P 500 are both pushing multi-year highs following through on a remarkably consistent climb originating back at the beginning of September (notably around the same time the Fed decided to maintain the size of its balance sheet and later to increase it). However, fundamentals do come into play. The S&P is at its richest valuation in six months; and the earnings seen recently conflict with the outlook for economic activity going forward. |  Risk is a relative measure. For short-term traders, this final week of the year is exceptionally risky because the reduced speculative interest in the system creates excessive volatility. On the other hand, higher levels of activity doesn’t translate into the development of significant trends. Another side effect of this year-end effect are reduced levels of implied volatility (generally, the cost of insurance against substantial losses). That said, a steady decline in the traditional measures of risk alongside a passive climb in underlying markets should be viewed as exceptionally risky. This is just a scenario where the market is ignoring and underpricing risk. It is not a stretch to suggest that is the case here given fundamental threats. |

Written by: John Kicklighter, Currency Strategist for DailyFX.com

To receive John’s reports via email or to submit Questions or Comments about an article; email jkicklighter@dailyfx.com

DailyFX provides forex news on the economic reports and political events that influence the currency market.

Learn currency trading with a free practice account and charts from FXCM.

Learn currency trading with a free practice account and charts from FXCM.

No comments:

Post a Comment