http://www.dailyfx.com/forex/fundamental/article/special_report/2010/12/29/A_Lack_of_Conviction_in_FX_and_Equities_May_Signal_a_Major_Impending_Reversal.html

There has been a remarkable divergence in the performance of the FX and other capital markets (equities, commodities, etc) in the past few months. Reduced correlations are normal during periods of thin speculative interest like we are experiencing now in the final weeks of the year; but this particular deviation can be traced back further than just the year-end liquidity drain. Most traders recognize the concept that the markets can only stray from fundamentals for so long before they snap back to a fair value. That same concept is applicable to the relationship between price action and participation. Risk appetite can climb without the full support of the retail and speculative market participant; but such a condition won’t last for very long.

To better understand participation, we need to break the market’s activity into two rudimentary parts: direction and momentum. Direction is the aspect that most traders concern themselves with; but momentum is arguably the more important ingredient to successful trading. A practical definition of momentum is the pace of follow-through on any given trend. However, that loose explanation does not fully encompass the value of this facet of trading. Perhaps more illuminating is the more straightforward description that it is the level of conviction in a prevailing move. For example, when we look at a long awaited breakout on a reversal; there is the initial volatility that is associated with panicked position covering. Yet, for this shift to truly translate into a meaningful reversal and trade setup; we need meaningful buying (or selling if it is bearish) interest to sustain a trend.

If we were to believe in the prevailing bullish trends from equities and commodities since the beginning of September, we would expect to see speculative interest support the persistent climb. In fact, we see in volume (one of the most basic measures of interest) a very clear divergence over the past four months and even further. Taking a look at the daily chart of S&P 500 price action and volume below a distinct contrast between the activity levels that prevailed back when the markets were sliding in the second quarter versus the lack of conviction through the steady build through September.

S&P 500 Price and Volume (Daily)

Chart generated with Bloomberg Professional

Taking a bigger-picture perspective of the markets, the below weekly chart of the S&P 500 shows diminished conviction in the recovery for the equities market. Encouraged by the tail end of the worst financial crisis in recent history, selling pressure led to significant swells in volume. Yet, since the steady recovery began with the March 2009 reversal, volume has gradually cooled (best seen in the 26-week moving average).

S&P 500 Price and Volume (Weekly)

Chart generated with Bloomberg Professional

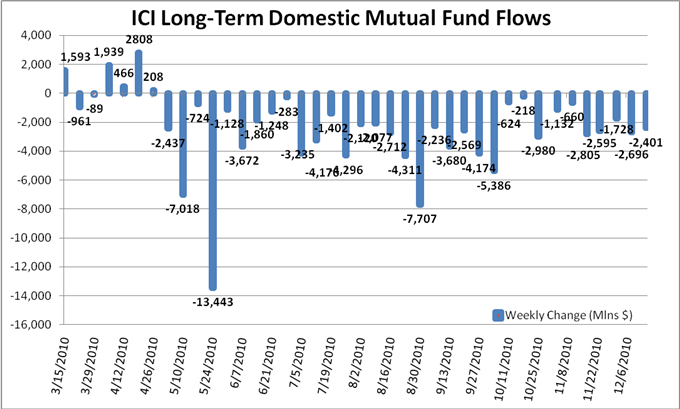

Just as surely as an extreme divergence between price action and an indicator like the MACD signals a high probability of reversal; so too does a remarkable deviation between speculative positioning and price action indicate ominous circumstances for a stable trend. It is very interesting to note that equity in long-term US mutual fund holdings (using data from Investment Company Institute) shows consistent outflows for 33 consecutive weeks. That gives a very different assessment of strength than mere price action alone provides. Other indicators measures can be used to measure interest as well including the Commitment of Traders report, the balance of open interest in options (calls versus puts) and the net short/long positioning index.

Source: Investment Company Institute

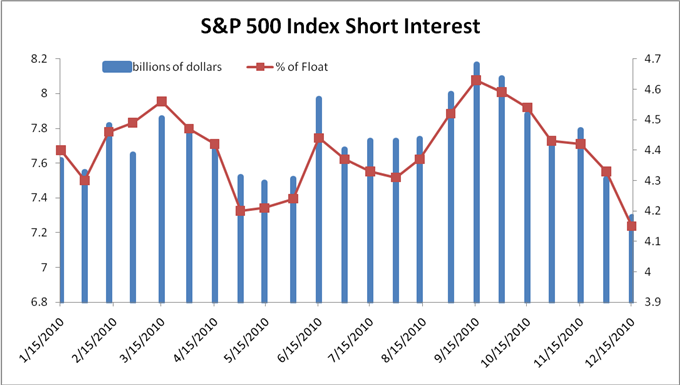

Heading into the end of the year, it becomes difficult to separate the influence of thinned speculative interest that is typical of the season from the ongoing effort to exit risky positions. In fact, looking at the total short interest in the S&P 500 Index, a progressive drop in bearish positioning (covering shorts) may actually be encouraging prices higher. That may seem bullish; but it is most likely temporary as traders are closing these positions to book losses for the tax season. If that is the case, this is a temporary booster for the market’s.

Heading into 2011, if bearish speculation is revived and the trend of diminished retail participation in risky assets persists; the burden of supporting such a celebrated bull trend will become impossible to bear. As the retail and institutional trader exits, bullish sentiment will become increasingly dependent on temporary factors such as government stimulus. And, such support cannot carry the markets for very long – much less survive a serious bout of speculative panic.

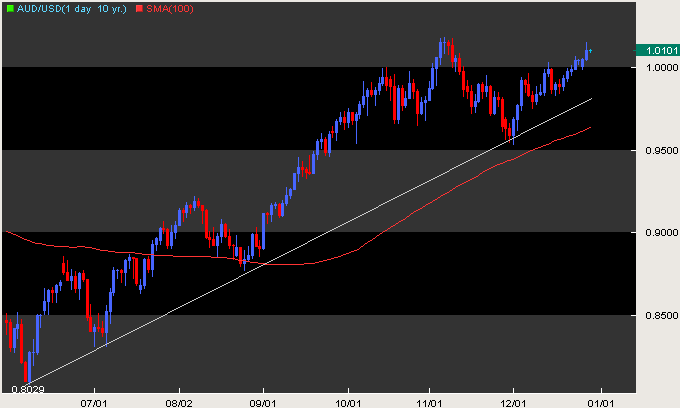

So, where does the FX market fit into this scenario? Amongst the most liquid pairs in the currency market, we have seen a far less conspicuous ‘padding’ of speculative interest. Notably, both EURUSD and GBPUSD are trading near the middle of their respective ranges for the year as risk appetite trends are overshadowed by more fundamental concerns (and in this case, perhaps EURUSD offers a better measure of ‘fair value’ than the distorted equities market). On the other hand, the artificial sense of risk appetite in capital markets distinctly carries over to pairs that are directed by carry interest. Therefore, one of the most exposed pairs for a potential reversal is AUDUSD.

Chart generated with FXTrek Intellicharts

The final condition of this potential reversal is timing. A particular catalyst such as an explicit deterioration in Euro-area financial health, the popping of a Chinese asset bubble or a fresh housing crisis in the US is a very real threat. However, the more influential spark for a market-wide drop in risky assets would be a swell in investor fear. The speculative herd is the largest faction in the market; and a concerted selling effort would easily overwhelm limited stimulus efforts. The first test of confidence will come over the opening two weeks of January. With the new investment year underway, traders will have to decide whether they are confidence enough in risk appetite to buy in at already rich levels.

Written by: John Kicklighter, Currency Strategist for DailyFX.com

To receive John’s reports via email or to submit Questions or Comments about an article; email jkicklighter@dailyfx.com

DailyFX provides forex news on the economic reports and political events that influence the currency market.

Learn currency trading with a free practice account and charts from FXCM.

Learn currency trading with a free practice account and charts from FXCM.

No comments:

Post a Comment