http://www.dailyfx.com/forex/fundamental/article/carry_trade_basket/2010/12/31/A_Falter_in_Risk_Appetite_in_2011_Could_Realign_the_Negative_Dollar_and_SPX_Correlation.html

- A Falter in Risk Appetite in 2011 Could Realign the Negative Dollar and S&P 500 Correlation

- How Long will it Take Liquidity to Fill Out and Markets to Reengage Genuine Trends?

- With a New Trading Year, Expect Market Participants to Reassess True Value

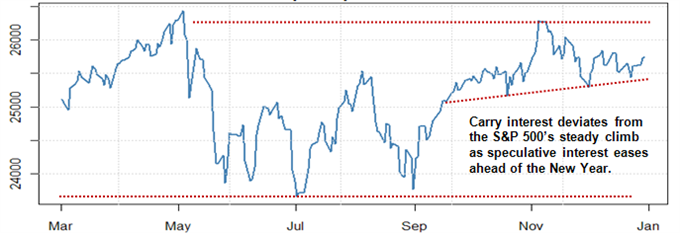

We are heading into the final trading hours of 2010. Looking back, it was a period less volatile than 2008 and less consistent (trend-wise) than 2009. Yet, heading into a new trading year; perhaps the most remarkable take-away from what has transpired is the divergence between prevailing market values and the fundamentals that should define speculative conviction. With the steady rise in the benchmarks for risk appetite (the S&P 500, the CRB Commodity Index and SPDR Capital High Yield Bond ETF among others), it would seem that the economic and financial scene is stable while the outlook for returns robust. However, the environment and data paint exactly the opposite picture. While the outlook for global growth is not exactly dire; few would argue against the assessment that it will be uneven, impeded by the inevitable withdrawal of stimulus, pained by the introduction of more austerity to rein in deficits and threatened by the potential of a few critical financial crises. To this point, the masses have been blissfully (or willfully) ignorant of the headwinds that face passive and optimistic investment. That said, reality will eventually contaminate this collective buoyancy; and the higher markets are at the point of inflection, the more dramatic the correction.

It is important to once and a while take a big picture view of the capital and speculative markets to garner a better understanding of what is driving price and when those factors have run their course. An often overlooked consideration is assessing who is responsible for the prevailing market winds. There are only a few classes of market participant that can exact a meaningful influence on current value. For the FX, equities and debt markets; the breakdown is made by those that have an economic agenda, speculators and the government (central banks). The flows through economic need exact a slow influence and are similarly sluggish to react. This is likely to remain the case through the near future given the outlook for economic activity and the reduced threat of financial emergencies. Traditionally, the government’s role is very limited; but at this point, it is extremely important. Tremendous amounts of stimulus have been pumped into the US, Euro Zone, Japan, China and other economies. One condition of this effort to stabilize markets and encourage growth is that the world has hit a point of diminished returns on further support as the impact to fiscal health will offset further iterations. The other aspect of this effort is that it the capital trickles down to assets and offers the speculative crowd an easy trade. Though there are exceptions, the markets are generally a zero sum game (where someone makes money another loses it). In this scenario, the speculator happily accepts the government’s money. And, accept the returns and concept they have – so much so that the S&P 500 is now at a two-year high while the AUDUSD is at a post float (28-year) high. That said, the party will end. Either traders will take profit in mass, a new financial trouble will override greed or stimulus will be removed.

These three scenarios are what we should look for to change the status quo. And, it is not a matter of ‘if’ this will happen, rather ‘when’ one of these developments will take place. The opening week of the year will struggle to restore liquidity. However, through January, investors will have a fresh slate to start from which to establish whether they want to allocate fresh funds to the markets. Considering how rich the markets are currently, the tipping point is likely near. And, if they don’t want to invest new capital, it will lead them to question why they don’t take profit. At this point, we are simply waiting for a catalyst. It doesn’t have to happen immediately, but soon…

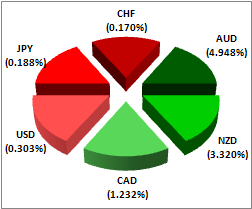

DailyFX Carry Trade Index

Risk Indicators:

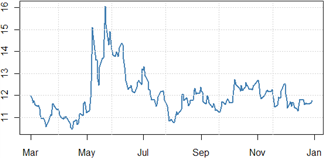

DailyFX Volatility Index

What is the DailyFX Volatility Index:

The DailyFX Volatility Index measures the general level of volatility in the currency market. The index is a composite of the implied volatility in options underlying a basket of currencies. Our basket is equally weighed and composed of some of the most liquid currency pairs in the Foreign exchange market.

In reading this graph, whenever the DailyFX Volatility Index rises, it suggests traders expect the currency market to be more active in the coming days and weeks. Since carry trades underperform when volatility is high (due to the threat of capital losses that may overwhelm carry income), a rise in volatility is unfavorable for the strategy.

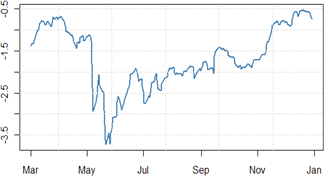

USDJPY 25 Delta Risk Reversals 3 Month

What are Risk Reversals:Risk reversals are the difference in volatility between similar (in expiration and relative strike levels) FX calls and put options. The measurement is calculated by finding the difference between the implied volatility of a call with a 25 Delta and a put with a 25 Delta. When Risk Reversals are skewed to the downside, it suggests volatility and therefore demand is greater for puts than for calls and traders are expecting the pair to fall; and vice versa.

We use risk reversals on USDJPY as global interest are bottoming after having fallen substantially over the past year or more. Both the US and Japanese benchmark lending rates are near zero and expected to remain there until at least the middle of 2010. This attributes level of stability to this pairs options that better allows it to follow investment trends. When Risk Reversals move to a negative extreme, it typically reflects a demand for safety of funds - an unfavorable condition for carry.

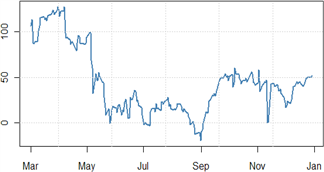

Reserve Bank of Australia Expectations

How are Rate Expectations calculated:

Forecasting rate decisions is notoriously speculative, yet the market is typically very efficient at predicting rate movements (and many economists and analysts even believe market prices influence policy decisions). To take advantage of the collective wisdom of the market in forecasting rate decisions, we will use a combination of long and short-term, risk-free interest rate assets to determine the cumulative movement the Reserve Bank of Australia (RBA) will make over the coming 12 months. We have chosen the RBA as the Australian dollar is one of few currencies, still considered a high yielders.To read this chart, any positive number represents an expected firming in the Australian benchmark lending rate over the coming year with each point representing one basis point change. When rate expectations rise, the carry differential is expected to increase and carry trades return improves.

Highest And Lowest Yields:

The Interest rate used to benchmark the currency basket is the 3 months Libor rate

Is Carry Trade and risk appetite rising or falling? Discuss how to trade yields and market sentiment in the DailyFX Forum

Additional Information

What is a Carry Trade

All that is needed to understand the carry trade concept is a basic knowledge of foreign exchange and interest rates differentials. Each currency has a different interest rate attached to it determined partly by policy authorities and partly by market demand.When taking a foreign exchange position a trader holds long position one currency and short position in another. Each day, the trader will collect the interest on the long side of their trade and pay the interest on the short side. If the interest rate on the purchased currency is higher than that of the sold currency, the result is a net inflow of interest. If the sold currency’s interest rate is greater than the purchased currency’s rate, the trader must pay the net interest.

Carry Trade As A Strategy

For many years, money managers and banks have utilized the inflow and outflow of yield to collect consistent income in times of low volatility and high risk appetite. Holding only one or two currency pairs would invite considerable idiosyncratic risk (or risk related to those few pairs held); so traders create portfolios of various carry trade pairs to diversify risk from any single pair and isolate exposure to demand for yield. However, even with risk diversified away from any one pair, a carry basket is still exposed to those conditions that render this yield seeking strategy undesirable, such as: high volatility, small interest rate differentials or a general aversion to risk. Therefore, the carry trade will consistently collect an interest income, but there are still situation when the carry trade can face large drawdowns in certain market conditions. As such, a trader needs to decide when it is time to underweight or overweight their carry trade exposure.

Written by: John Kicklighter, Currency Strategist for DailyFX.com

To receive John’s reports via email or to submit Questions or Comments about an article; email jkicklighter@dailyfx.

DailyFX provides forex news on the economic reports and political events that influence the currency market.

Learn currency trading with a free practice account and charts from FXCM.

Learn currency trading with a free practice account and charts from FXCM.

No comments:

Post a Comment