http://www.dailyfx.com/forex/fundamental/article/special_report/2010/12/31/Inflation_and_the_US_Dollar.html

http://www.dailyfx.com/forex/fundamental/article/special_report/2010/12/31/Inflation_and_the_US_Dollar.html

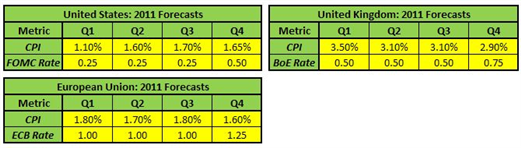

Despite the Fed’s policies of expanding the monetary supply indefinitely – not materially, but through large scale asset purchases – the inflation rate has yet to reach the central bank’s target of 2 percent over the medium term. Over the past 12 months, inflation has been slowly creeping upward, albeit at a slower pace than the Federal Reserve desires. The Consumer Price Index has risen 1.1 percent, while core PCE prices have risen approximately 1.2 percent over this same time frame. Given the current slack in the system – high unemployment and low capacity utilization – low inflation should be expected. That being said, inflation is expected to be 1.5 percent for 2011; and on a quarter-by-quarter basis, from first to fourth, respectively: 1.1 percent, 1.6 percent, 1.7 percent, and 1.65 percent.

When considering hedging against inflationary pressures with regards to trading the U.S. Dollar, it is important to consider when the Federal Reserve is anticipated by the market to increase interest rates. Market consensus, for now, sees the benchmark interest rate holding at 25 basis points through end of the third quarter, with a 25 basis points increase sometime during the fourth quarter. The Bank of England and the European Central Bank are forecasted to take similar routes: while the rates are different for these central banks, they both are expected to hold the main refinancing rate constant until the fourth quarter, when a 25 basis points increase is expected.

As currency traders know, interest rates, inflation, and exchange rates are highly correlated. If interest rates are expected to remain within the same yield differentials over the next four quarters, then differentials in inflation and interest rates can be used to forecast how the Dollar will move against other currencies such as the Pound and the Euro.

Primarily, what can be derived from inflation rate expectations and nominal interest rate expectations are real interest rate expectations, the rate of interest an investor receives after subtracting inflation. As noted by the tables above, the real interest rate among the United States, Great Britain, and the European Union are expected to be negative throughout 2011 – real interest rates for the United States, Great Britain, and the European Union have been negative for some time. Despite the Fed’s efforts towards expanding the monetary supply, which in theory should be increasing inflationary pressures, such has not occurred nor is expected to boost underlying consumer prices that greatly in the United States, according to market sentiment. Accordingly, the Federal Reserve has found little evidence to raise interest rates.

Over the next year, while interest rates hold, based on real interest rate differentials, one could forecast for the Dollar to gain against the Pound, while the Euro offers a higher rate of return than the Greenback over the same time frame. However, as inflationary pressures rise in the United States, and as the Federal Reserve is forced to raise the main refinancing rate, the Dollar could become a more attractive currency option, and draw the attention of foreign investment, leading to a Dollar appreciation across all of the major currency pairs.

Written by Christopher Vecchio, DailyFX Research

To discuss this report contact Christopher Vecchio:cvecchio@fxcm.com

DailyFX provides forex news on the economic reports and political events that influence the currency market.

Learn currency trading with a free practice account and charts from FXCM.

Learn currency trading with a free practice account and charts from FXCM.

http://www.dailyfx.com/forex/fundamental/article/special_report/2010/12/31/Inflation_and_the_US_Dollar.html

No comments:

Post a Comment